ITIF, a US-based nonprofit, nonpartisan research and educational institute, was founded in 2006. A major area of concern for ITIF is ‘America’s competitive position in advanced technologies and industries that constitute the most strategically important sectors of the economy.’ To undertake focused research in this area, the Institute created the Hamilton Center of Industrial Strategy. One of the main mandates of this Center is to research and advocate appropriate strategies to policymakers to keep America the numero uno in emerging technologies and overcome the challenge posed by China. This Center has been publishing an index called the Hamilton Index of Advanced-Technology Performance, to track global shares of value-added output in 10 advanced industry sectors across 40 countries. These industries include Pharmaceuticals; Fabricated Metals, Basic Metals, Electrical Equipment; Machinery and Equipment; Motor Vehicles, Other Transportation; Computer and Electronics, Information Technology and Information Services; and Chemicals (excluding pharmaceuticals)

The 2000 data used for index computation is given below

Industry

Global Output Billions

Leading producer

Leader’s share

IT and Information Services

$1,900

USA

36.40%

Computers and Electronics

$1,317

China

26.80%

Chemicals

$1,146

China

29.10%

Machinery and Equipment

$1,135

China

32.00%

Motor Vehicles

$1,093

China

24.30%

Basic Metals

$976

China

45.60%

Fabricated Metals

$846

China

25.60%

Pharmaceuticals

$696

USA

28.40%

Electrical Equipment

$602

China

36.10%

Other Transportation

$386

USA

34.50%

Total

10.1 trillion

It is evident that China is a potential challenger to US supremacy in technology and, consequently, military dominance worldwide. When US technology companies like Apple rushed to China to take advantage of cheap labor, no one could have imagined that China was working on technology assimilation by unbundling the underlying technology stacks, chip by chip. It is now too late for the US President to force Apple to invest $500 billion in the USA. Apple has already been disrobed

The top ten countries accounted for 75% of the total global production, valued at $10.1 trillion. China’s share was around 25% of the global output of these technology-intensive industries, slightly more than the combined share of the rest of the world outside the top ten producers. Although India had a larger workforce, its advanced industry produced only 13% of China’s output.

The ITIF is betting that China will not achieve the level of innovation capability that the USA and its allies have reached since the end of World War II. However, this hope could be a mirage that may never lead to an oasis. Finally, what about India? This will be a story that will end with:

Mr. Rahul Gandhi, the current leader of the opposition in the Indian parliament, has made a clarion call to fight against the Indian State. This has created a huge backlash, accusing him of treason. Now, these words—Nation, State, and Government—are often used very casually in everyday conversation. The present author is also not aware of the deep nuances of these three abstract terms and how their abstractions have played out in reality. I did not find it feasible to undertake a deep study of these concepts. Therefore, I sought the help of AI—Copilot and Chat GPT. The answers I got are quite interesting. In this Blog, I am reproducing the answers given by these two AI applications. I am also including a few quotations from one or two articles / books suggested by the AI tools.

Question: What is the definition of Nation?

Answer:

Chat GPT- Defining the concept of a “nation” is complex because it encompasses various dimensions — political, cultural, historical, and social — and different scholars may emphasize different aspects. However, a broadly accepted definition of a nation is:

A nation is a large group of people who share a common identity, culture, language, ethnicity, or history, and who typically inhabit a specific territory, and may seek political sovereignty or self-determination.

Key Components of This Definition:

Common Identity: Nations are often defined by shared aspects of identity, such as ethnicity, culture, language, religion, or historical experiences.

Territory: A nation is often tied to a specific geographic area or homeland, though the extent of that territory can vary.

Political Aspiration or Sovereignty: While not all nations are sovereign states, many nations seek or have sought self-determination or political autonomy.

Shared Culture/History: Nations are often united by a common culture or a collective memory of historical events, struggles, or achievements.

Nation vs. State: A “nation” is a social and cultural concept, while a “state” refers to a political entity with sovereignty and recognized borders. A nation may or may not coincide with a state (e.g., the Kurds are a nation but do not have an independent state of their own).

Ethnicity and Nationalism: National identity can be linked to ethnicity, but it can also transcend ethnic boundaries (e.g., the idea of “American” identity encompasses many different ethnic groups).

This broad definition allows for various forms of nations, including those without independent political control (e.g., the Palestinians) or those that are part of larger political entities (e.g., the Catalans in Spain).

Though this definition is widely accepted, debates continue on its nuances, especially around the roles of language, ethnicity, and shared culture in defining a nation, particularly in multicultural societies or regions with competing national identities

Copilot- The concept of a nation is multifaceted, but it generally refers to a large group of people who share common elements such as language, culture, ethnicity, history, and sometimes religion. These shared characteristics create a sense of collective identity and belonging. Here are a few key points

Shared Identity: Members of a nation often feel a sense of unity and pride based on shared characteristics and experiences.

Territorial Boundaries: Nations typically have defined geographical boundaries, though these can sometimes be disputed.

Sovereignty: A nation may seek or possess political sovereignty, meaning the authority to govern itself without external interference.

Common Goals and Values: Nations often have common aspirations and values, which can be political, social, or economic.

Historical Continuity: Many nations trace their identity back through a continuous historical narrative.

In short, a nation is a community with a sense of shared identity, culture, and often a desire for political autonomy. The modern nation-state combines this idea of a nation with a defined territory and government

Question- What is the definition of State?

Answer:

Chat GPT – A widely accepted and concise definition of a state is:

A state is a political entity with a defined territory, a permanent population, a system of government, and the capacity to enter into relations with other states.

Key Components of This Definition:

Defined Territory: A state has clearly established geographic boundaries recognized by others.

Permanent Population: A state is home to a stable population, though the exact number or demographic composition can vary.

System of Government: The state has an organized political structure (such as a democracy, monarchy, dictatorship, etc.) that governs and enforces laws.

Sovereignty: A state possesses sovereignty, meaning it has the supreme authority within its borders and is not subject to the control of external powers.

Distinctions:

A state is distinct from a nation, though the two can overlap (e.g., a nation-state like Japan).

A state may not always be a nation, as a state can encompass multiple nations or ethnic groups (e.g., India, the United States, or Belgium).

This definition captures the basic political and legal characteristics that are commonly used to recognize a state in the international system.

Copilot – The concept of a state is also multifaceted and can be defined in several ways. Here are some key elements that generally characterize a state:

Territory: A state has defined geographical boundaries.

Population: A state has a population that resides within its territorial boundaries.

Government: A state has an organized political structure that exercises authority over its territory and population.

Sovereignty: A state possesses sovereignty, meaning it has the ultimate authority within its borders and is not subject to external control.

Legal System: A state has a legal system that governs the behavior of its population and administers justice.

Recognition: A state is often recognized by other states and international organizations, which can grant it legitimacy on the global stage.

In essence, a state is a political entity that has a defined territory, a permanent population, a government, and the sovereignty to make and enforce laws within its borders.

Question- What is the definition of Government?

Answer:

Chat GPT – The concept of a state is also multifaceted and can be defined in several ways. Here are some key elements that generally characterize a state:

Territory: A state has defined geographical boundaries.

Population: A state has a population that resides within its territorial boundaries.

Government: A state has an organized political structure that exercises authority over its territory and population.

Sovereignty: A state possesses sovereignty, meaning it has the ultimate authority within its borders and is not subject to external control.

Legal System: A state has a legal system that governs the behavior of its population and administers justice.

Recognition: A state is often recognized by other states and international organizations, which can grant it legitimacy on the global stage.

In essence, a state is a political entity that has a defined territory, a permanent population, a government, and the sovereignty to make and enforce laws within its borders.

Copilot – The concept of government refers to the system or group of people governing an organized community, typically a state. Here are some core aspects of government:

Authority and Control: Government exercises authority and control over a specific territory and its population.

Institutions: It consists of institutions, such as the executive, legislature, and judiciary, which perform various functions.

Law and Order: Government enforces laws to maintain order and provide security for its citizens.

Public Services: It provides essential services like healthcare, education, and infrastructure.

Taxation and Budgeting: Government collects taxes and allocates resources to fund public services and infrastructure.

Representation: In democratic systems, government represents the will of the people, often through elected representatives.

Policy Making: It formulates and implements policies to address social, economic, and political issues.

In essence, government is the structure and process through which a society organizes itself, makes decisions, and enforces rules and policies to achieve collective goals

Question – What are the differences between Nation, State and Government?

Answer-

Chat GPT Summary of Differences:

Concept

Focus

Nature

Key Features

Nation

Cultural and social identity

People and identity

Common culture, language, ethnicity, and history. Not tied to political control.

State

Political entity

Legal and territorial

Sovereign territory, government, laws, and international recognition.

Government

Political organization and leadership

Administration of the state

Group of people and institutions that make and enforce laws.

Example to Illustrate:

The United States:

Nation: A collective identity shaped by shared cultural, historical, and political experiences, including the concept of “American” identity.

State: The United States as a political entity with clearly defined borders, a constitution, and sovereignty recognized internationally.

Government: The U.S. Government, which consists of elected officials (e.g., the president, congress, judiciary) who make decisions and enforce laws for the country.

In essence, the nation refers to the people with shared identity, the state refers to the political and legal structure governing a territory, and the government refers to the specific group or system of leaders and institutions managing the state’s affairs.

Copilot

Key Differences

Nature: A nation is a social and cultural concept, a state is a political and legal entity, and a government is an organizational structure.

Focus: Nations focus on identity and culture, states focus on political boundaries and sovereignty, and governments focus on administration and governance.

Interrelations: A state can encompass multiple nations (like the United Kingdom), and a nation can exist without a state (like the Palestinians). Governments operate within states to manage and govern.

Question- When does state collapse to Government?

Answer–

Chat GPT – In an autocracy, especially in a totalitarian regime like Nazi Germany, the state and government can become merged in practice, as the leader holds absolute power over both the nation’s sovereignty and its administration. While there is still a theoretical distinction (the state being the permanent sovereign entity and the government being the machinery that runs it), in autocratic regimes the leader’s authority often collapses the two into one, making the difference between the state and government less significant or practically nonexistent.

Copilot -The concepts of state and government can overlap or be seen as the same in specific contexts, usually in cases of authoritarian regimes or highly centralized governments. Here are a few scenarios:

Totalian Regime: In totalitarian regimes, the state and the government are often indistinguishable. The ruling government exerts complete control over all aspects of political, social, and economic life, making the state’s identity synonymous with that of the government. Examples include North Korea and former Soviet Union under Stalin

Highly Centralized States: In some highly centralized states, where local and regional governments have minimal power, the central government may be seen as the embodiment of the state. China is an example, where the Communist Party’s control over the government largely defines the state.

Lack of Distinction in Language : In some contexts, especially in everyday language, people may use “state” and “government” interchangeably. While technically different, this can blur the lines between the two concepts.

However, it’s important to note that in most democratic and federal systems, the distinction between the state (as the broader political entity) and the government (as the current administration) is maintained to ensure checks and balances.

Question- Is it true that Nations are a recent phenomenon?

Answer:

Chat GPT The concept of a “nation” as we understand it today — a group of people united by shared identity, culture, language, and often governed by a single political entity — is a relatively modern development, emerging particularly in the 17th and 18th centuries with the rise of the nation-state. However, looking back through history, some ancient groups or entities can be seen as precursors to modern nations based on shared culture, identity, and governance. Here are a few that might qualify.

The closest early examples of what could be considered “nations” in an ancient sense are Ancient Egypt and Ancient Israel, where a shared culture, religion, and political structure created a strong, unified identity. While the idea of a “nation-state” as we know it didn’t exist in ancient times, these groups exhibited many of the characteristics we associate with nations today, such as shared identity and centralized governance

Copilot Nations, as we understand them today, are considered a relatively recent phenomenon1. The concept of a nation-state, where a distinct group of people with shared characteristics such as language, culture, and history form a political entity, became prominent only towards the end of the 18th century.

Before this period, people primarily identified with smaller kinship groups, tribes, or territorial authorities. The idea of nationalism, which ties the concept of a nation to a specific state, really took off during and after the French Revolution

End of Question and Answer.

Finally, let me quote from an article by Benedict Anderson, the author of Imagined Communities. In this article, using Indonesia as an example, he underlined two common mistakes that most people make about nationalism.

The first is that nationalism is something very old and is inherited from, of course, “absolutely.” Thus, it is something that arises “naturally” in the blood and flesh of each of us. In fact, nationalism is something rather new, and today is little more than two centuries old.

The second misunderstanding is that “nation” and “state” are, if not exactly identical, at least like a happy husband and wife in their relationship. But the historical reality is often just the opposite. Perhaps 85 percent of nationalist movements started life as movements aimed against colonial or feudal-absolutist states. Nation and state “got married” very late on, and the marriage was far from always happy. The general rule is that the state-or what in my circle of friends we often call the Spook-is much older than the nation

Note: Andersons’s article- Indonesian Nationalism Today and in the Future

Every storm runs out of rain eventually- Maya Angelou

A storm has erupted across the streets of India following an invoking of the name of Babasaheb Ambedkar in a derogatory manner by the Home Minister. This happened when a discussion was going on in Rajya Sabha to commemorate the 70th anniversary of the Indian Constitution. Babasaheb, to recall, was the chairman of the drafting committee of the independent India’s constitution. No doubt, this storm will also pass. However, the idea and vision of Babasaheb will remain unread, gathering dust in the library of the parliament. Ironically, both the ruling party and the opposition are earnestly praising a man by attributing to him ideas and beliefs that stand diametrically opposed to those of the Babasaheb who aspired to create a truly democratic and secular India after colonial rule.

To understand what Babasaheb Ambedkar stood for, we need to read a definitive exposition of his thoughts in the text of the speech he composed but could not deliver. In December 1935, the “Jat-Pat-Todak Mandal” (translated as the Society for the Breakup of the Caste System), a reformist organization in Lahore, invited Babasaheb to deliver a speech on the Indian caste system at their annual conference scheduled for January 1936 in Lahore. After he shared the first draft of the speech (Ambedkar 1935) with the conference organizers, a difference of opinion arose over certain views expressed in that draft. Since neither the author nor the organizers were willing to compromise on their positions, Babasaheb withdrew the speech. The title of the speech was “Annihilation of Caste,” and ironically, the inviting organization, while opposed to the caste system, advocated for breaking the barriers between castes rather than its complete annihilation, a goal for which Babasaheb was fighting. To understand the intellectual underpinnings of this dispute and the current controversy, we must recognize the critical difference between these two views.

Why social reform is necessary for political reform? (Section 2 of the speech)

Babasaheb Ambedkar was clear about the pre-eminence of social reform over political reform. By “social reform” he meant elimination of “mischiefs wrought by evil customs” prevailing in the Hindu society which was not “in a state of efficiency”, and “ceaseless efforts must be made to eradicate these evils”. The goal of political reform is to eradicate “the weak points in the political organization in the country”. Babasaheb was of the opinion that without the prior occurrence of social reform, political reform would be a non sequitur, rendering it of no value to the people of the country. He pointed out that two organizations, namely National Congress and Social Conference, were twins at their birth – the first one to spearhead political reform while the other one to social reform. However, “in the course of time the party in favour of political reform won, and the Social Conference vanished and was forgotten.” For Babasaheb, it was a conscious move by Hindu liberals. To underscore this point, he highlighted the following lines from a speech delivered by the president of the National Congress at its eighth session held in Allahabad in 1892:

“I for one have no patience with those who say we shall not be fit for political reform until we reform our social system. I fail to see any connection between the two. Are we not fit (for political reform) because our widows remain unmarried and our girls are given in marriage earlier than in other countries? because our wives and daughters do not drive about with us visiting our friends? because we do not send our daughters to Oxford and Cambridge? (Cheers [from the audience])”.

To reinforce and hammer away his contention that without social reform, political reform would provide no succor to the people who have been treated as animals for millennia, Babasaheb referred to a variety facts about the inhuman treatment that the untouchables of Hindu society receive from the upper caste people. He emphasized that by social reform, he does not mean the reform of the ‘Hindu family’, like abolition of child marriage, allowing widow marriage etc. He was seeking the reform of the fundamental architecture of the Hindu society- that is abolition of the Caste System.

Why social reform is necessary for economic reform (section 3 of the speech)

In this section, Babasaheb argues that even a socialist revolution in India would fail without effecting social reform prior to it. To prove his point that political policymaking can have “value and permanence” if and only if it is in conformity with existing social practice within a society, he referred to many such instances from the history. However, more importantly, he referred to the “Communal Award” which was created on 16 August 1932 by the British government of India, to extend separate electorate to Depressed Classes (called Scheduled classes in Independent India) and other minorities. This shows that the British Government understood that without this limited social reform, even a small political reform would be a non-starter. Although Mahtma Gandhi and National Congress was vehemently opposed to eking out a separate electorate from Hindu community, Babasaheb welcomed heartily this policy of the British government of India. It is worthwhile to quote what Mahatma Gandhi wrote about this British policy.

They do not realize that the separate electorate will create division among Hindus so much so that it will lead to bloodshed. Untouchable hooligans will make common cause with Muslim hooligans and kill caste Hindus. Has the British Government no idea of all this? I do not think so. (Duncan Ira , 2022, also see Helen M. Nugent (1979))

Babasaheb was unconcerned about the merits or demerits of socialism because his entire life was singularly focused on eradicating the most inhuman evil of Hindu society—caste. To quote him- “This is only another way of saying that, turn in any direction you like, Caste is the monster that crosses your path. You cannot have political reform, you cannot have economic reform, unless you kill this monster.”

It is more than evident that Dr. Ambedkar’s view about the fundamental and unchangeable social hierarchy of the Hindu society was widely different from the views of the Congress leadership. Despite this, he agreed to be the one of the main architect of the independent India’s constitution because the Congress leadership agreed to provide a separate electorate for Scheduled Castes and Tribes. In other words, as a pragmatic leader, he believed that a bird in the hand is worth two in the bush. This act of him does not imply that he had given up his lifelong struggle for annihilation of caste.

Caste is not just a division of labour, it is a division of labourers (section 4 of the speech)

Apologists of the caste system argue that it should be viewed, ignoring its etymological past, as another name for the modern division of labor, which is an integral part of any industrial society. Babasaheb , while accepting the division of labour as one of the attribute of the caste system, points out that the caste system of the Hindu society also determines an hierarchy in that division of labour, condemning those at the bottom as not worthy to be treated as an independent human being. The division of labor based on skill, dexterity, and judgment does not, in principle, determine the purported division at the time of a person’s birth. This sui generis division of labor is essentially a division of laborers, argues Babasaheb. The age old Indian division of labour based on caste system has thus led to “subordination of man’s natural powers and inclinations to the exigencies of social rules.”

Caste cannot preserve a nonexistent “racial purity”( section 5)

In today’s world the “racial purity” is just a fantasy , harbored by many but followed by none. Maintenance of “racial purity” could have been a motivation for the authors of Manusmrity, but to hallucinate it today is a non-sequitur. In this regard, we may look at the statement issued by the American Association of Physical Anthropologists in the year 2019. “pure races, in the sense of genetically homogenous populations, do not exist in the human species today, nor is there any evidence that they have ever existed in the past.” . In view of this declaration, one cannot but agree with Babasaheb’s view about the claim of racial purity for themselves by the upper caste Hindus: “[the caste system] embodies the arrogance and selfishness of a perverse section of the Hindus who were superior enough in social status to set it in fashion, and who had the authority to force it on their inferiors.” (Last para )

Caste prevents Hindus from forming a real society or nation ( section 6)

As a critique of Hinduism, Babasaheb has no equal so far. His criticism is not merely a scholarly investigation into a social construct, unwrapping of interplay of power, property and social status, layer by layer. Rather, it is the result of felt agony of being an untouchable in a highly fractured and rigidly hierarchical society. Nevertheless, he actively participated in the nation building effort of independent India by providing his deep knowledge about Indian society, modern jurisprudence and structure of governance in advanced countries. Therefore, the point arises, why he should be so skeptical about the possibility of independent India becoming a modern nation without any spec of ignominy of untouchability for any section of the society. In this regard, the following quote, a lengthy one, is good enough to understand the rationale behind his views.

In every Hindu the consciousness that exists is the consciousness of his caste. That is the reason why the Hindus cannot be said to form a society or a nation.

Men do not become a society by living in physical proximity, any more than a man ceases to be a member of his society by living so many miles away from other men

The similarity in habits and customs, beliefs and thoughts, is not enough to constitute men into society

Men constitute a society because they have things which they possess in common. Parallel activity, even if similar, is not sufficient to bind men into a society

The Caste System prevents common activity; and by preventing common activity, it has prevented the Hindus from becoming a society with a unified life and a consciousness of its own being.

This is a very radical view about what constitutes a society or a nation. If we consider all the above points with regard to a country like USA, it would have failed to qualify as a nation until mid-20th century. The Rosa Park event happened on December 1, 1955 at the capital of Alabama. City busses in that city followed the law of segregation- the front seats for whites and the rest for blacks. Ms. Park, after a busy day boarded a city bus and sat in the middle, just behind the front “white” section. When incoming passengers filled up the front white section, the bus driver ordered the black passengers in the middle row to vacate the seats and stand. Rosa Park refused. She was arrested and convicted for defying the segregation law. It is a different matter that this event led to quashing of segregation law.

Let us recall the “ I have a dream “ speech of Martin Luther King that he delivered on the steps of Lincoln Memorial of Washington DC on August 23, 1963. To recall, around 100 years back, the US president Abraham Lincoln had signed the Emancipation Proclamation freeing the slaves.

I have a dream today.

I have a dream that one day down in Alabama, with its vicious racists, with its governor having his lips dripping with the words of interposition and nullification; that one day right down in Alabama little black boys and black girls will be able to join hands with little white boys and white girls as sisters and brothers.I have a dream that one day this nation will rise up and live out the true meaning of its creed. We hold these truths to be self-evident that all men are created equal

By Babasaheb’s yardstick, USA could not be called a nation.

In fact, inequality is all pervasive. The only difference between India and USA is that the dominant religion in USA does not discriminate between white and black people, per se. No Church would disallow a black to pray in its sanctuary. However, an untouchable is routinely denied entry into the sanctuary of many famous Hindu temple- called Garbhagriha.

Although majority of Indians are Hindu and Hindus by themselves do not form a society for reasons enumerated byBabasaheb Ambedkar in this section of his speech. But for that reason India does not cease to be a nation. However, Babasaheb. Ambedkar’s argument will become valid, if India ceases to be a secular country and Indian Constitution is amended to declare it as Hindu Rashtra.

The worst feature of the Caste System is an anti-social spirit (section 7)

The anti-social spirit is a phenomenon that cuts across castes, religions and languages. In every nation or society, it would be difficult not to find a small community or a group that live at the margin of the society and called anti-social. Babasaheb himself has written this in the second para of this section: “This anti-social spirit, this spirit of protecting its own interests, is as much a marked feature of the different castes in their isolation from one another as it is of nations in their isolation.”

Similarly, the British Government of India enacted Criminal Tribes Act (CTA) 1871 to notify certain tribes as criminal and kept them under continuous surveillance, thus labelling about 200 communities in several provinces “criminal” communities under this act (Devy 2013 Ram Singh).

In Great Britain, a large survey of ethnic minority groups was carried out in 2021. According to a Guardian report the survey has revealed that ethnic minorities Roma, Gypsy and Traveller face extremely high levels of racial assault, poor health, precarious employment and socioeconomic deprivation. The research found that 62% of Gypsy or Traveller people had experienced a racial assault. In other words, although anti-social spirit is present in all nations, Indian system of caste may make it more pervasive ( see the link in reference section below)

Caste prevents the uplift and incorporation of the aboriginal tribes ( section 8)

This section essentially repeats section 7, with the only difference being that it focuses on aboriginal tribes, referred to as ‘scheduled tribes’ in the Indian Constitution. He criticizes the Hindu society for ignoring 13 million people still “living in the midst of civilization … in a “savage state”. The reason for this apathy of a Hindu towards anyone born outside the caste system is that Hindus are more concerned about protecting the purity of his or her caste. Unlike a Christian missionary, Hindu priests rarely engage themselves in proselytization, as it would be difficult to assign any particular caste to the converted person because caste is determined at birth only. That is why, a number Hindu groups are against worshiping Sai Baba, because he was born a Muslim.

Remaining sections

The higher castes have conspired to keep the lower castes down (section 9)

Caste prevents Hinduism from being a missionary religion (section 10)

Caste deprives Hindus of mutual help, trust, and fellow-feeling (11)

Caste is a powerful weapon for preventing all reform (section 12)

Caste destroys public spirit, public opinion, and public charity (section13)

I want to address all five sections in one go because they are interrelated and repetitive, highlighting one of the most important shortcomings of Hinduism: its rigidity and the consequent barrier to conversion from other faiths to Hinduism. Dr. Ambedkar views Hinduism as a constellation of castes, where internal unity is highly fragile and contingent upon any dire external threat. This exclusivity of Hinduism is not on

ly directed at non-Hindus but also manifests within its own people by creating an insurmountable hierarchy of status, privileges, occupation, and socialization among believers.

The following quotes from Dr. Ambedkar’s un-delivered lecture proves the point.

The Hindus criticise the Mohammedans for having spread their religion by the use of the sword. [But] Hindu would not spread the light,…would endeavour to keep others in darkness, [and], would not consent to share his intellectual and social inheritance” with others who are ready to consider conversion to Hinduism. I have no hesitation in saying that if the Mohammedan has been cruel, the Hindu has been mean; and meanness is worse than cruelty. (Last para of section 9 )

Hindu Society being a collection of castes, and each caste being a closed corporation, there is no place for a convert(Last para of section 10)

With the Hindu Gods all-forbearing, it is not difficult to imagine the pitiable condition of the wronged and the oppressed among the Hindus. Indifferentism is the worst kind of disease that can infect a people. Why is the Hindu so indifferent? In my opinion this indifferentism is the result of the Caste System, which has made Sanghatan and co-operation even for a good cause impossible.(Last para of section 11)

Caste in the hands of the orthodox has been a powerful weapon for persecuting the reformers and for killing all reform. (Last line of section 12)

The capacity to appreciate merits in a man, apart from his caste, does not exist in a Hindu. There is appreciation of virtue, but only when the man is a fellow caste-man. The whole morality is as bad as tribal morality. (Last para of section 13)

I believe that the above summary of the five paragraphs faithfully presents the views of the respected doctor. Despite having experienced inhuman treatment at the hands of upper-caste Hindus, Babasaheb, setting aside his personal rancor, has provided a succinct and accurate description of the caste system in Hinduism. However, criticism is a lazy exercise for any great thinker of the stature of Babasaheb. People would like to know: What is the road ahead? Will it be possible to annihilate the caste system in Hindu society within the next hundred years?

In this respect, Babasaheb has only left for his followers only a dream—a dream similar to the one Martin Luther King articulated in 1963. King’s dream has largely remained unfulfilled, and fate has so far played the same game with Babasaheb. In this speech, Babasaheb outlines his vision for a society based on liberty, equality, and fraternity. The great French revolutionary Robespierre suggested that these words be inscribed on the flags of France in 1790. They were denied, and after a few failed efforts, they were incorporated into the French Constitution of 1948.

After spelling out his ideal, in the next 11 sections of the speech, Dr. Ambedkar gave detailed reasons for the impossibility of Hindu society accepting and implementing his ideals. So far, efforts to bring reform from within the Hindu society, keeping the caste system intact, with some marginal tweaking, has failed as it was inevitable given the basic structure of Hindu religion. In this respect, Babasaheb was right. In the last section, he expressed his frustration through the title of the section itself- The struggle is yours; I have now decided to leave the Hindu fold.

Babasaheb wrote this speech in December 1935 and Dr. Ambedkar adopted Buddhism on October 14, 1956. It took him two decades to take the plunge because he could not or did not want to be a Godless person. To be an atheist and leader of any community in India, even if that community is untouchable to its other communities worshiping the same God, is next to impossible. This is the same reason for accepting a key position in the committee for drafting of the Indian constitution. He did not want to give any leeway to other members of drafting committee to incorporate Hinduism in that precious document. In this respect at least, he had Pandit Nehru as a co-believer. I believe it was Pandit Nehru’s masterstroke to bring in the Doctor as the head of the drafting committee. Otherwise ,there was a possibility that Mahtma Gandhi’s view about the eternal sanctity of Hindu Dharma could have found place in the constitution.

When Babasaheb took upon himself to publish his speech, Mahatma Gandhi entered into a debate with the doctor by pointing out fallacies in Babasheb’s train of argument. A perusal of text of that debate clearly shows that there was no meeting ground between the two.

The article so far has pointed out the deep divergence between the understanding of Congress about Hindu Dharma and that of Babasaheb. What about BJP’s view on this subject? I can only say that Babasaheb Dr. Bhimrao Ambedkar must be laughing in the heaven, subject to its existence, if BJP is ready to chant his name in praise. May be, the sun has started rising in the west.

Bhimrao Ambedkar must be laughing in the heaven, subject to its existence, if BJP is ready to chant his name in praise. May be, the sun has started rising in the west.

Finally, we must accept that an overwhelming majority of Indian people are deeply religious, and very few are willing to renounce their ancestral religion. At the same time, a significant section of Hindus is not ready to follow all dictates of the Shastras or Manusmriti and would actively support any effort towards the annihilation of caste. We must find a middle path to gradually break the stranglehold of Brahmins and high-caste people on the practice of Hindu religion. A list of low-hanging fruits is given below.

For any government document, the caste title like Sharma, Bhat, Upadhyay, Chatterjee, Iyer, Shastri, Chattopadhayay, Bagchi, Pandit etc. will be forbidden. Mother’s given name should follow every person’s given name and nothing more. Father’s name must not be part of this naming convention.

This naming convention would apply to all government documents including property registration document, birth certificate, passport etc.

UPSC should prepare a list of qualified priests, based on open examination. All temples must select priests from this list. People should consider Priesthood as any other job which, requiring specific skill- like knowledge of Satras etc. Every university should have a degree in priesthood also.

Implementation of the above list of aspirational activities may not be easy and vehement opposition to its’ introduction will defiantly break out. However, Rome was not built in one day.

References:

Ambedkar, Bhimrao Ramji (B.R) , 1935 The Annihilation of Caste, Columbia Centre for Teaching and Learning https://ccnmtl.columbia.edu/projects/mmt/ambedkar/web/readings/aoc_print_2004.pdf

Duncan Ira 2022, Ambedkar and British Policy on the Communal Award: A Response to Sujay Biswas , Studies in People’s History, 9, 2 (2022): 224–240 : quoted from M.K. Gandhi, ‘Appendix: Discussion on the Communal Award, 21 August 1932’, CWMG, Vol. 56, p. 466

Fuentes A, Ackermann RR, Athreya S, et al. AAPA statement on race and racism. Am J Phys Anthropol 2019;169:400–402.

Helen M. Nugent (1979) The communal award: The process of decision‐making, South Asia: Journal of South Asian Studies, 2:1-2, 112-129

Adam Smith began his magnum opus “An Inquiry into the Nature and Causes of the Wealth of Nations”, with the following line:The annual labour of every nation is the fund which originally supplies it with all the necessaries and conveniences of life which it annually consumes. (Smith- 1776; EBC edition 2001: Book 1 page 12)

For a given amount of labour, according to Smith, the wealth of a nation will on the productivity of that labour. While there is no inherently intrinsic level of productivity of a human being, it can be worked upon and enhanced by appropriate organizational structure, technological initiatives and incentives. According to Smith, the “greatest improvement in the productive powers of labour, and the greater part of the skill, dexterity, and judgement with which it is anywhere directed, or applied, seem to have been the effects of the division of labour.”(op.cit. page 17) It is not that the nature’s bounty – land, water, and environment- does not give a head start to a particular nation, but it would not make a nation wealthier if the “skill, dexterity, and judgment” and “division of labour” are not well developed and do not become an integral part of the production system.

Notwithstanding Smith’s identification of “labour” as the source of all wealth, he was pragmatic enough to understand that a market economy is not designed to bring the maximum benefit to providers of labour that creates wealth. In fact, he was aware that a market economy, per se, has no institutional mechanism for reduction of inequality in distribution of a nation’s wealth, and, therefore, it cannot bring about more equality in distribution of initial endowment of wealth that provides enormous advantage only to a small minority of people. His main concern was the growth of an economy- a growth that critically depends on the increase in productivity of labour. He had no illusion about the antagonistic nature of relation between wage earners and profit earners. Smith, an astute observer of social power structure and author of Theory of Moral Sentiments, understood the real mandate of any civil government:

Civil government, so far as it is instituted for the security of property, is in reality instituted for the defence of the rich against the poor, or of those who have property against those who have none at all (Smith: op.cit. Book 5 page 953)

This article shows that, even after 250 years of Smith’s assertion that labour is the ultimate source of wealth, the share of a nation’s wealth remains concentered in the hands of rich. The remit of all civil governments and international organizations remain the same- to enforce and maintain the inequality in wealth and power within and without a nation.

Definition of wealth

Etymologically, the English word “wealth” traces its ancestry to the old English “weal” and before that to “wel”. Both these words referred to a general state of “wellbeing “. The circularity in this definition notwithstanding, for people at large, possession of material “wealth” is both necessary and sufficient condition for a person’s wellbeing. In order to measure wealth in possession of an individual, family or a community, we need to identify valorized components of wealth. Irving Fisher, in his book, “The nature of capital and income” , defined and elucidated the term “wealth” in a market economy in the following manner.

The term ” wealth” is used in this book to signify material objects owned by human beings. According to this definition, an object, to be wealth, must conform to only two conditions: it must be material, and it must be owned. To these, some writers add a third condition, namely, that it must be useful. But while utility is undoubtedly an essential attribute of wealth, it is not a distinctive one, being implied in the attribute of appropriation; hence it is redundant in a definition. (Fisher 1906,page 3).

For Fisher ownership of material goods is a necessary qualification of a material object to be considered as a part of a legal entity’s wealth. He clarified this with following examples:

Rain, wind, clouds, the Gulf Stream, the heavenly bodies — especially the sun, from which we derive most of our light, heat, and energy — are all useful, but are not appropriated, and so are not wealth as commonly understood. (op.cit page 3)

More than one hundred years have passed since Fisher gave his definition of wealth. Today, even clean air is not only a desirable but a precious material object too. According to UN Environmental Program, air pollution is the greatest environmental threat to public health globally and accounts for more than 8 million premature deaths every year. A number of recent empirical studies have shown that polluted air has a negative impact on labour productivity and thereby on human capital component of a nation’s wealth (see Chen and Zhang 2021). Thus, measured degradation in the quality of environment needs to be considered as a liability that must be deducted from the value of asset. It also highlights the complexity and contradictions in the concept of ownership , especially when accounting for environmental impact. For example, access to natural resources like living and non-living useful objects in sea has been demarcated with a national boundary based on international agreement and are always prone to conflicts between nations. Similarly, the question of whether possession equates to ownership is a complex legal issue. When Smith or even Fisher wrote about wealth, they did not have to deal with the issue of ‘knowledge as a source of wealth”. For them “skill, dexterity” of individual workers, combined with “judgement” of entrepreneurs created wealth.

It is quite evident that the concept of wealth is as fuzzy as its equivalent concept of wellbeing. The definitional issues of ‘wealth” is beyond the scope of this article, although measurement of “wealth” of a nation would depend on the demarcation of the underlying definitional boundary. Since there is no globally accepted definition of wealth of a nation, for this study, we have used two well recognized datasets on national wealth- one by the World bank that provides wealth data from 1995 to 2018 and another one by the Credit Suisse (now UBS) that provides data on household wealth since 2000. Credit Suisse (now UBS) is a globally active financial institution having a very large wealth management practice. Although we take a quick over view of wealth measured across nations, our focus is on three largest nations- China, India, and USA. (Reference part of this article gives the details of all reports of these two agencies)

Box 1 Data Quality

The two datasets that we have used for our evaluation of distribution of wealth, across the nations and within a nation, are subject to many qualifications. A brief discussion of the most important ones follows. The World Bank calculates the present value of future flows of produced outputs generated by land, labour and capital – that is a country’s GDP- by using a time-independent discount factor uniformly for all nations. This approach may introduce inaccuracies since each country’s economic conditions vary from country to country. On the other hand, the Credit Suisse /UBS evaluates household wealth, which includes “financial assets and real assets (principally housing)” using market value, wherever available, (see Notes on concepts and methodspage 19 of 2023 UBS report). However, due to the volatility of financial markets, price movements in one country may not align with those in others, leading to inconsistent valuations across countries. At the country level, domestic currency is typically used for valuation of assets, but for international comparisons, a conversion to a common currency is required. The World Bank does this by using market exchange rates in constant 2018 US dollars. The Bank also looked at how using Purchasing Power Parity (PPP) based exchange rates affects this measure. When using PPP, the share of global wealth for low-income and lower-middle income countries rises from 7.3% to 15.8%. The Credit Suisse/UBS used end period market exchange rate to convert local currency estimates into US dollar-based estimates. The price volatility, degree of market dominance by a few large corporates etc. are key features that vary from market to market. Such variations is far from negligible and in the absence of any normalization of data across markets, its impact on the wealth distribution data remains unaddressed. Apart from measurement issues, wealth data even at national level is fraught with a number of conceptual issues, particularly concerning definitional boundary of Natural Capital and Human Capital. For example, the assessment of a country’s natural wealth depends on available knowledge about resources located within its recognized borders. These borders are determined according to international agreements, and any limitations in resource knowledge can affect wealth calculation. In spite of having many data such quality issues, the two data sets used in this article are the only ones that provide complete coverage of wealth of nations over a reasonably long time.

Estimation methodology of National Wealth by the World Bank:

Components of wealth:

Where is the wealth of nations? (World Bank 2006) was the first attempt by the Bank to provide “comprehensive snapshot of wealth for 120 countries at the turn of the millennium”. Since 2006, the Bank is publishing a yearly report titled The Changing Wealth of Nations: Managing Assets for the Future (CWON). This article uses data published in the 2021 report, the latest available.

To measure a nation’s wealth, the World Bank relies on two closely related international standards for valuing economic activity within national borders. The first standard is the System of National Accounts (SNA), which focuses on national income measurement. The United Nations Statistical Commission (UNSC) released the first version of SNA in 1953, with the latest update in 2008. The SNA bases its accounts on transactional data related to production, consumption, and the accumulation of assets. The institutional units participating in these exchanges within a market economy generate this data.

The System of National Accounts (SNA) defines an asset as “a store of value.” Any rent or profit generated from this asset must accrue to the “economic owner” in the future. Following the principles of Irving Fisher, the SNA does not consider any store of value without identifiable economic ownership as an asset. (page 39 para 3.5 SNA 2008). Following Irving Fisher, SNA also does not recognize any store of value that has no identifiable economic ownership, as an asset.

The second standard, introduced in 2012 and used by the Bank, is the System of Environmental-Economic Accounting (SEEA), which is the accepted international standard for environmental-economic accounting. The SEEA framework acknowledges the inherent link of every production system to its surrounding environment, and its significant impact on all production activities by human beings. These environmental impacts include the depletion of natural, non-produced resources, such as forests, minerals, and air, as well as a reduction in the quality of environment, which ultimately undermines the production process itself. The concept of sustainability in growth stems from the recognition that the environment may eventually be unable to sustain such production levels. In terms of accounting principles, conventions, and table structures, the SEEA aligns with the SNA.

The core premise of the World Bank’s methodology is that a nation’s wealth consists of three major types of assets or capital: produced assets, natural capital, and human resources. Human resources include raw labor, human capital, and the intangible yet essential element known as social capital (World Bank 1997, Page 19). An outline of the definitions and boundaries for each of these components follows.

Produced Assets:

SNA 1993 defined “produced assets” as “non-financial assets that have come into existence as outputs from processes that fall within the production boundary of the SNA; produced assets consist of fixed assets, inventories and valuables.” Thus, human capital, and natural resources without any identified owner are excluded (Paragraphs 10.7 and 13.14, see also SNA 2008 page 48 para 3.49)

Three types of produced non-financial assets are:

Fixed assets,

Inventories, and

Valuables, which include items like precious metals, antiques, and art objects.

Non-produced assets comprises of three sub-groups:

Natural resources,

Contracts, leases, and licenses, and

Goodwill and marketing assets.

Natural Capital

Natural capital comprises of three principal categories: natural resource stocks, land and ecosystems. Natural resources are non-renewable resources like oil, natural gas, coal and mineral resources. Land includes cropland, pastureland, and forested areas. Ecosystem assets are those assets, which provide ecosystem services that are essential for sustainability of any human society. In environmental accounting, ecosystem incorporates both living organizations and the physical environment encompassing them in a specific area comprising landscape as well as seascape (see Estelle Dominati et al 2010, United Nations 2003). The CWON 2011 report provides further details about these Ecosystem Services and measurability of them. (CWON 21 page 22)

Human Capital

The three attributes of labour, namely “skill, dexterity, and judgement” are the main drivers of labour productivity. The income that a laborer earns in her lifetime can be considered as “flow of rents (or economic profits) in the future.”(page 3 CWON 2011). Accordingly, the Bank measures Human Capital as the present value of all future labour income (2021 CWON report page 144).

Box 2 Genuine Savings Wealth, in the form of produced assets, increases through savings and investment. Net national savings are calculated by subtracting the consumption of fixed capital from the gross national savings, as per the System of National Accounts (SNA). Consumption of fixed capital reflects the depreciation of productive capacity during the estimation period. This measure of net national savings, however, does not account for the sustainability of economic growth, as it overlooks changes in natural resource bases and environmental quality besides produced assets (as highlighted in “Expanding the Measure of Wealth,” page 8). Consequently, the value depletion of natural resources like energy, metals, minerals, and net forest stocks is estimated and subtracted from the net national savings. Since education enhances human capital, current expenditures on education are added to the net national savings. This adjusted figure is known as genuine savings. Many natural resource-dependent countries exhibit low or negative genuine savings, indicating long-term sustainability issues.

Measurement of wealth

From the perspective of sustainability of current economic growth, measurement of wealth at a time t needs to be the sum of all future consumption, appropriately discounted on future consumption path. Symbolically, this has been written as: where Wt is the present value of future flows of income in the year t, C(S) the is the consumption in a future year s , and r is the social return to investment or the discount factor for future benefits. The Bank has taken 24 years as the time horizon for its wealth computation. As regards the social discount factor, 4 per cent has been used. The Bank has not provided any counterfactual study with regard to these assumptions. However, comparison of change in wealth across nations may not suffer from gross errors, provided that the degree of errors is bounded across nations. Similarly, a nation’s income as measured by GDP represents the cash flows generated from the produced wealth of the nation. Essentially, estimating a nation’s produced wealth becomes straightforward with an assumed income (i.e. GDP) growth rate and a given discount factor. The World Bank data is available from 1995 to 2018. For a given year, the total wealth is the sum of the following components:

Total wealth = renewable natural capital + nonrenewable natural capital+ produced capital + human capital + net foreign assets. Data given in 2021 CWON is in constant USD 2018, at market exchange rate. All data has been sourced from https://datacatalog.worldbank.org/dataset/wealth-accounting

Estimation methodology of Household Wealth by Credit Suisse/ UBS

Credit Suisse, a Switzerland-based global investment bank, was established in 1856. Since 2010, the bank has been publishing the Global Wealth Report (GWT), which provides profiles of household assets across various nations. An accompanying publication, titled the Global Wealth Databook, offers detailed data that underpins the main report. In March 2013, Credit Suisse was acquired by another Swiss bank, UBS, in an all-stock deal orchestrated by a joint effort of the Swiss government and the Swiss Financial Market Supervisory Authority, to prevent the potential fallout from a Credit Suisse bankruptcy. UBS has continued publishing the Global Wealth Report since 2023. The latest report was published in July 2024.

In contrast to the World Bank’s approach, GWT estimates wealth solely at the household level. At this level, net worth, or ‘wealth,’ is defined as the market value of financial and non-financial assets owned by a household, minus any debt. Real assets consist primarily of housing properties owned by households. This approach does not include human capital, natural capital, or other elements considered in the World Bank’s method for measuring national wealth. Additionally, government or community-owned assets are excluded (see Davies et al). To ensure consistency in measuring wealth across nations, all asset valuations are converted to US dollars using the end-period exchange rate. For assessing the wealth of individuals at the top end of the distribution in each country, the data is adjusted using wealth estimates given by in the Forbes list of billionaires.

Wealth of Nations – World Bank estimates

Between 1995 and 2018, global wealth increased from 603.5 trillion USD to 1152.5 trillion USD- indicating a compounded growth rate of 3.4 %. Only in two years- 2006 and 2007, the growth rates were more than 4%. The composition of wealth remained more or less the same during this period. During the same period, the Global GDP at constant 2015USD increased by a compound growth rate of 3.1%. The average shares of three major components, Produced Capital, Natural Capital and the Human Capital – remained at around 51.5%, 6.7% and, 62% respectively (see annexure table A2.1 and A2.2).

The global wealth is concentrated in two high-income group of countries, namely OECD and non-OECD countries. Non-OECD high-income countries, such as the UAE and Bahrain, have a very low population share, only 1% in 2018. As a sub-group, their share in total wealth remained between 2% to 3%. Although high-income OECD countries continue to hold the largest share of the world’s total wealth, their share declined from 74.3% to 58.3% between 1995 and 2018. During the same period, their corresponding population share also declined modestly, from 17.6% to 15%. Lower middle-income countries, including India, accounted for the highest share of the world’s population in 2018 (39.7%) but held a very modest share of the world’s total wealth (5.7%). Human capital was the largest source of wealth for most countries, except for high-income non-OECD and low-income countries. The share of natural capital in total wealth was the lowest for high-income OECD countries, at a mere 2.1%. This suggests that the bounty of nature is neither necessary nor sufficient for the generation of wealth (see Table A2.3). Data on country wise shares in wealth and population shows that the top ten countries in terms of their wealth in 2018 have hardly changed between 1995 and 2018. The entry of China in this club of rich countries has compensated for the decline in the share of High-income OECD countries. These top ten countries accounted for around 72% of total global wealth and around 55 percent of the world’s population. The most important takeaway from these estimates of national wealth is the phenomenal rise of China. In 1995, China’s wealth was only 22 percent of USA’s wealth and by 2018, it has reached to 85%. During this period, the ratio of China’s population to that of USA remained almost the same- 4.5 in 1995 to 4.3 in 2018 (see Table A2.6). The shares of China, India, and USA in the total wealth of the world, given below, shows how China has leapfrogged to become the wealthiest country of the world.

Table 1: Wealth Share versus Population Share of countries

Year 2000

Year 2010

Year 2018

National Wealth Band

Share in World Population

Share in Wealth of the World

Share in World Population

Share in Wealth of the World

Share in World Population

Share in Wealth of the World

less than 1 trillion

13.5%

2.7%

13.8%

2.6%

12.4%

2.3%

1-5 trillion

21.0%

10.9%

20.9%

9.9%

18.4%

6.9%

5-10 trillion

7.1%

7.2%

1.8%

4.2%

7.4%

0.0%

10 – 50 trillion

29.7%

29.6%

36.5%

33.8%

35.0%

27.7%

More than 50 trillion

28.8%

49.6%

27.0%

49.5%

26.8%

56.8%

World Bank Data

China’s increasing footprint in the world economy is not only consistent with its growth in its national wealth but also with the growing prosperity of its average citizen. Thus, the per capita GDP growth rate of China during the period 1995 -2023 remained well above the corresponding growth rates of India as well as USA. The data given below corroborates this.

Table 3: Growth in per capita GDP of China/India/US

Per capita GDP- Compound Growth Rate

China

India

USA

1960-1970

2.4%

3.0%

5.7%

1970-1980

5.6%

9.1%

9.2%

1980-1990

5.0%

3.3%

6.6%

1990-2000

11.7%

1.8%

4.3%

2000-2010

16.8%

11.8%

3.0%

2010-2020

8.6%

3.6%

2.8%

2020-2023

6.6%

9.1%

8.3%

2023 GDP as ratio of US GDP

0.15

0.03

1

World Bank Data

Wealth of Nations – Credit Suisse/ UBS estimates

The 2024 Global Wealth report estimates 4.2 % increase in global wealth ( in USD) in 2023 as compared to a decline of (-)3% in 2022. The report has highlighted that in the last 15 years of publication of this report only 3 times there has been a decline in the estimated global wealth in USD term- “during the financial crisis of 2008, in 2015 and once again in 2022, when both equities and bonds dropped across all major markets” ( page 5).

Table 4 Distribution of Global Household Wealth- 2022

Wealth range ( in thousand USD)

No of adults (million)

No of adults (%)

Total wealth in Trillion)

Wealth percentage

less than 10K

2818

52.5

5.3

1.2

10K-100K

1844

34.4

61.9

13.6

100K-1million

642

12.0

178.9

39.4

>1 million USD

59.4

1.1

208.3

45.8

Source:Global Wealth Report 2023 page 22 and Table 3-1: Wealth pattern within markets, 2022 in Global Wealth Databook 2023

The wealth distribution for China, India, and USA, countries in focus of this article shows that India stands apart from the other two most populous countries.

Table 5: Wealth Distribution of Adults for the China, India , and USA -2022

Wealth range ( in thousand USD)-

Distribution of no of adults (%)

China

India

USA

less than 10K

19.3%

73.8%

17.5%

10K-100K

65.6%

24.0%

30.3%

100K-1million

14.5%

2.1%

43.2%

>1 million USD

0.6%

0.1%

9.0%

Gini Coefficient of wealth distribution

70.9%

82.5%

83.0%

Note: 10K USD would be little less than 10 lac Indian rupees. A person with even 1 acre of agricultural land in rural India would have more than 10 lac worth wealth.

Finally, we find that acute wealth-deprivation of 90% of Indian people has made no adverse impact on the rising wealth of 1% of people at the top of the pyramid of wealth. In fact, between 2002 and 2018 the share of the top 1 % of India’s wealth owners have increased from 15.7% to 18.3%. At the same time, the share of the bottom 90% of wealth owners hovered around 47%. For both China and USA, there has been similar increase in inequality in distribution of wealth.(see the table A2.13 ).

In a market economy, financial wealth is the dominant form of total wealth of households. In China, the share of financial wealth has increased from 36.4% to 45.4 % between 2000 and 2022. During the same period, the share of the financial wealth in the gross wealth held by Indian households decreased from 24.1% to 21.0%. The share of financial wealth in the gross wealth of households in USA hovered around 68% during the same period.(see Table A2.14)

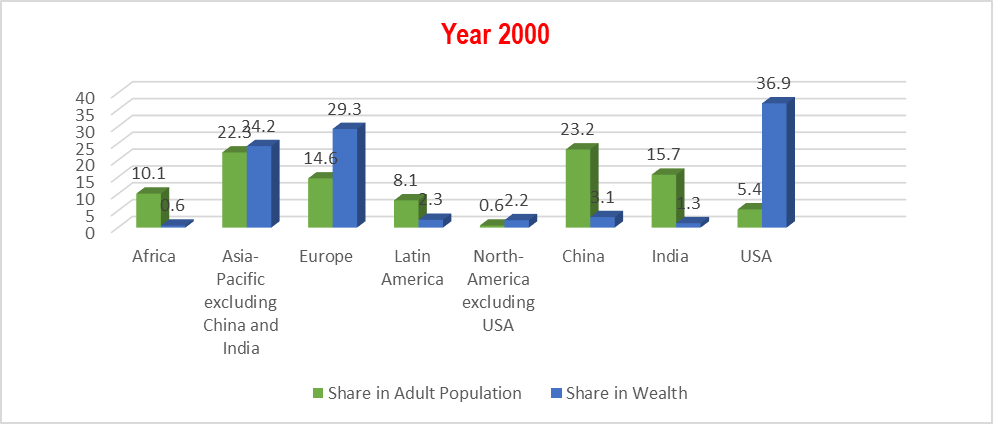

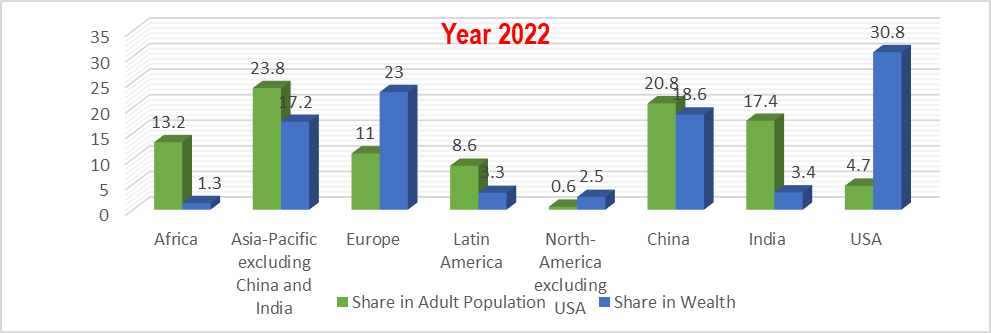

The regional distribution of household wealth shows that world continues to remain highly unequal. In the year 2000, Africa, Latin America and India together accounted for 33.9% of the adult population of the world and only 4.2% of household wealth of the world. In the same year, the corresponding shares of Europe and USA together were 20% and 66.2 percent. By 2022, the share in total adult population did not change much for the first group, but its share in the wealth almost doubled from 4.2% to 8%. For the second group, both the shares declined to 15.7% and 53.8% respectively (see the Annexure Chart 1). The most remarkable fact about the changing distribution of the world’s wealth is the phenomenal rise of China’s wealth share. It increased from 3.6% in 2000 to 18.6% in 2022- a fivefold increase. During the same period, China’s share in adult population decreased from 23.2% to 20.8%.

One noteworthy feature of growth of household wealth in this millennium is the drastic fall in growth rate between two decades for some selected markets. The Annexure table A2.10 shows that annual compounded growth rates for household wealth has more than halved for many important countries between 2000-10 and 2010-23. For example, the household wealth growth rate (compounded annually) of Russia declined from 20% in the first decade to only 4% in the next period of 13 years. The corresponding figures for China and India were (19,8) and (14,7) respectively. The comparable growth rate for USA was 4 and 6 respectively.

Billionaires of the world with special reference to China. India and USA

Forbes, an USA based business magazine, publishes every year a global list of US dollar billionaires. The magazine published its first list in 1987. Between 1987 and 2024, the number of billionaires in the world have increased from 470 to 2781, with their net worth having increased from $898 billion to $14.9 trillion. A comparison with total household net wealth published by UBS shows that the share of billionaires in total household wealth increased from 1.42% in 2005 to 2.8% by 2022. (See the chart).

In India, 166 billionaires own 4.9% of total household wealth of India in the year 2022, while the corresponding numbers for China and USA are 2.3% and 3.4% respectively.

UBS in collaboration with PWC has also been publishing a report on billionaires of the world since 2015. covering mostly 43 markets in the Americas, Europe, the-Middle East and Africa (EMEA) and Asia-Pacific. In 2023, UBS/PWC study covered 2544 billionaires as against 2376 in the previous year. The report provides an interesting insight into the persistence of wealth in an already wealthy family. During the study year 2023, 53 multi-generation billionaire inherited USD 150.8 Billion, while 84 new first generation billionaires were worth of USD 143.7 Billion. ( UBS 2023, page 24 Section 2 )

The main conclusion that we can safely draw from the data assembled in this article is that the distance between elites and the poor in terms of opportunity dominance within a given society of Homo sapiens has not changed noticeably, from the times when our ancestors started accumulating wealth. Annexure 3 provides a brief discussion of inequality prevailing in such ancient human societies that existed between 11000 to 2000 years ago.

Annexure 1 Charts

Chart1: Share of Regions and 3 most Populous countries in the world’s adult population and wealth (in %)

Source : Global Wealth Databook 2023 UBS

Chart 2: Number of Billionaires of the World- and their share in the World’s Wealth

Table A2.1: Income group wise share in global wealth and population

Year

1995

2010

2018

Income Group

Share in total wealth

Share in population

Share in total wealth

Share in population

Share in total wealth

Share in population

High income: non-OECD

2.18%

0.77%

2.82%

0.96%

2.64%

1.05%

High income: OECD

74.32%

17.64%

64.02%

15.88%

58.26%

15.01%

Low income

0.49%

5.78%

0.53%

7.24%

0.59%

8.26%

Lower middle income

4.98%

36.29%

6.11%

38.77%

6.73%

39.72%

Upper middle income

18.04%

39.52%

26.52%

37.14%

31.78%

35.96%

Table A2.2 : Share of various wealth types for different income groups– Year 2000

Income Group

Share of Produced Capital

Share of Natural Capital

Share of Human Capital

Share of Net Foreign Assets

High income: non-OECD

18%

34%

38%

10%

High income: OECD

34%

2%

65%

0%

Upper middle income

27%

13%

60%

-1%

Lower middle income

27%

19%

58%

-3%

Low income

26%

39%

39%

-3%

Note: Row percentages are in relation to total wealth of the corresponding income group.

Table A2.3: Share of various wealth types for different income groups– Year 2010

Income Group

Share of Produced Capital

Share of Natural Capital

Share of Human Capital

Share of Net Foreign Assets

High income: non-OECD

17.7%

42.2%

31.9%

8.2%

High income: OECD

35.9%

2.8%

62.0%

-0.6%

Upper middle income

23.6%

13.9%

62.4%

0.0%

Lower middle income

24.5%

18.3%

59.3%

-2.1%

Low income

25.8%

34.2%

41.7%

-1.8%

Note: Row percentages are in relation to total wealth of the corresponding income group.

Table A2.4: Share of various wealth types for different income groups– Year 2018

Income Group

Share of Produced Capital

Share of Natural Capital

Share of Human Capital

Share of Net Foreign Assets

High income: non-OECD

23.2%

30.8%

33.6%

12.4%

High income: OECD

35.0%

2.1%

63.8%

-0.8%

Upper middle income

25.8%

7.9%

66.2%

0.1%

Lower middle income

27.2%

13.5%

62.1%

-2.8%

Low income

27.7%

25.6%

50.0%

-3.3%

Note: Row percentages are in relation to total wealth of the corresponding income group.

Table A2.5: Average growth rate of total wealth for five-year period by regions

Year

East Asia & Pacific

Europe & Central Asia

Latin America & Caribbean

Middle East & North Africa

North America

South Asia

Sub-Saharan Africa

World

1995-2000

3.91

1.75

2.40

2.50

3.75

4.60

0.49

3.01

2001-2005

4.08

1.63

2.55

5.22

1.71

5.22

3.27

2.51

2006-2010

5.73

1.73

3.87

6.57

1.05

6.14

6.94

3.05

2011-2015

5.34

1.29

3.47

3.75

1.78

5.46

4.26

3.04

2016-2018

4.31

1.76

1.31

-2.31

1.71

5.90

1.85

2.54

Note: South Asia includes India. East Asia and Pacific includes China. North America includes USA. Middle East and North Africa includes Saudi Arabia, Iran and Israel. Total wealth is calculated as the sum of produced capital, natural capital, human capital, and net foreign assets. Values are measured at market exchange rates in constant 2018 US dollars, using a country-specific GDP deflator.

Table A2.6 Share in total global wealth and population for top ten countries in terms of wealth in 2018.

Country

1995

2000

2010

2018

Share in Wealth

Share in Population

Share in Wealth

Share in Population

Share in Wealth

Share in Population

Share in Wealth

Share in Population

United States

30.10%

4.89%

31.41%

4.84%

27.05%

4.69%

24.73%

4.74%

China

6.69%

22.11%

8.49%

21.48%

15.20%

20.22%

21.07%

20.75%

Japan

10.52%

2.28%

9.68%

2.16%

7.25%

1.92%

6.14%

2.02%

Germany

6.45%

1.49%

5.86%

1.40%

5.09%

1.21%

4.84%

1.30%

France

4.44%

1.09%

4.25%

1.04%

3.66%

0.98%

3.29%

1.01%

United Kingdom

3.63%

1.06%

3.72%

1.00%

3.17%

0.95%

2.85%

0.98%

India

1.50%

17.84%

1.66%

18.26%

2.26%

18.81%

2.83%

18.52%

Canada

2.95%

0.54%

2.85%

0.53%

2.79%

0.52%

2.64%

0.52%

Russian Federation

2.99%

2.69%

2.56%

2.48%

2.61%

2.15%

2.17%

2.30%

Brazil

2.53%

2.99%

2.35%

3.01%

2.45%

2.97%

2.13%

2.98%

Total

71.80%

56.98%

72.83%

56.21%

71.54%

54.42%

72.69%

55.11%

Table A2.7: Comparison of three selected countries in terms of per-capita wealth

Country Name

Per capita 2000

Rank

Ratio to Median

2010 per capita

Rank

Ratio to Median

2018 per capita

Rank

Ratio to Median

United States

779093

6

18.4

804679.9

5

13.3

872400

6

13.7

China

47046

72

1.1

104563.4

52

1.7

174365

41

2.7

India

10972

121

0.3

16875.8

118

0.3

24102

110

0.4

Note: Rank and Median are based on per capita wealth of 146 countries.

Table A2.8: Share in Total Wealth of the World by three largest countries in terms of population

Country

1995

2000

2010

2018

China

6.7%

8.5%

15.2%

21.1%

India

1.5%

1.7%

2.3%

2.8%

USA

30.1%

31.4%

27.0%

24.7%

Total

38.3%

41.6%

44.5%

48.6%

A2.9: Average growth rate of total wealth for 5 year period by regions

Year

East Asia & Pacific

Europe & Central Asia

Latin America & Caribbean

Middle East & North Africa

North America

South Asia

Sub-Saharan Africa

World

1995-2000

3.91

1.75

2.40

2.50

3.75

4.60

0.49

3.01

2001-2005

4.08

1.63

2.55

5.22

1.71

5.22

3.27

2.51

2006-2010

5.73

1.73

3.87

6.57

1.05

6.14

6.94

3.05

2011-2015

5.34

1.29

3.47

3.75

1.78

5.46

4.26

3.04

2016-2018

4.31

1.76

1.31

-2.31

1.71

5.90

1.85

2.54

Source- World Bank. 2021. The Changing Wealth of Nations 2021

Credit Suisse / UBS Data

Table A2.10 Comparison of wealth growth rates over time

Country

2000-10

2010-23

Russian Federation

20

4

Mainland China

19

8

UAE

16

4

Brazil

15

3

India

14

7

Indonesia

13

6

South Africa

13

2

France

10

2

Italy

7

minus 0

Germany

6

3

Japan

6

minus 2

UK

5

4

USA

4

6

Table A2.11: Wealth per adult

Country

GDP per adult (USD)-2021

Wealth per adult 2000 USD)

Wealth per adult (USD) 2022

Total wealth 2022 USD Billion

Share in global wealth 2022

China

15,624

4,247

75,731

84,485

18.6

India

3,561

2,643

16,500

15,365

3.4

USA

100,380

215,146

551,347

139,866

30.8

UBS : Global Wealth Databook 2023 page 20-22