The difference between fiat money like the US Dollar and Bitcoin is comparable to the difference between the US Dollar and gold. The global supply of gold increases as new gold is mined, just as the mining process determines the supply of new Bitcoin. Like gold, people buy, hold, and sell Bitcoin largely in pursuit of capital gains. Today, cryptocurrencies are primarily viewed as investment assets rather than everyday mediums of financial transactions.

Currently, the total value of Bitcoin in circulation is about 19.91 million BTC (≈ 1.6816 trillion USD). In comparison, the estimated above-ground stock of gold is around 216,215 tons, valued at approximately 23.5 trillion USD. Therefore, it is anybody’s guess as to how long it will take Bitcoin to become the most preferred way to be a store of value. Interestingly, 45% of the world’s gold is held in the form of Jewelry- a feat beyond the capacity of bitcoin. This is because “ Gold is unbelievably beautiful” ( Why do we value gold? By Justin Rowlatt)

As the ownership of gold is highly skewed, the same is true of Bitcoin. It is interesting to know that the highest ownership of Bitcoin as an individual is none other than Satoshi Nakomoto, an unknown person or a group of persons going by this pseudonym, who invented Bitcoin in October 2008. The total Bitcoin held under this name is around 1.1 million BTC, across 22000 wallets. The market value of this holding is around 93 billion dollar as on April 2025. The skewed distribution of this digital asset can be seen from the following table.

Conclusion Bitcoin, like gold, demonstrates both its appeal as a store of value and its tendency toward concentrated ownership. While its future role in global finance remains uncertain, its distribution patterns suggest that Bitcoin is not unlike other scarce assets—valuable, but unevenly held.

I am trying to understand the concept and use cases of blockchain. I plan to put up a series of blogs on this subject as I navigate through the complexity of the subject. I will be more than happy to receive any response pointing out flaws in my understanding. Please write to me at ashok.nag@gmail.com.

Definition of Blockchain:

Bitcoin.org: The blockchain is a shared public ledger on which the entire Bitcoin network relies. All confirmed transactions are included in the blockchain. It allows Bitcoin wallets to calculate their spendable balance so that new transactions can be verified thereby ensuring they’re actually owned by the spender. The integrity and the chronological order of the blockchain are enforced with cryptography.

Ethereum: A blockchain is a public database that is updated and shared across many computers in a network.

Wikipedia: A growing list of records, called blocks, that are securely linked together using cryptography. The blocks are timestamped and chained with the previous block by incorporating a cryptographic hash of the previous block.

IBM: Blockchain is a shared, immutable ledger that facilitates the process of recording transactions and tracking assets in a business network.

Oracle: Blockchain is defined as a ledger of decentralized data that is securely shared. Blockchain technology enables a collective group of select participants to share data. With blockchain cloud services, transactional data from multiple sources can be easily collected, integrated, and shared. Data is broken up into shared blocks that are chained together with unique identifiers in the form of cryptographic hashes.

Our definition: Blockchain is a digital record management system with the following properties:

Records are grouped into blocks with a pre-defined limit for the size of a block. The size of a block determines the number of records of a given size that a block can include. Data in blocks can only be appended and not deleted or modified.

The process of creating a new block and adding it to a given chain determines the type of blockchain. There are mainly two types of blockchain, namely permissionless and permissioned. The former one is called public blockchain as access to it is open to all. The latter type restricts access to authenticated users only and is also known as a private blockchain.

Blocks are mostly stored in a key-value database. Bitcoin, Ethereum, and many other cryptocurrencies use LevelDB database of Google. Cryptographic hashes are used as identifiers for a block as well as its records. In other words, hashes are the keys and the data as the value.

The “chain” part in “Blockchain” refers to the fact that two consecutive blocks are linearly linked as a parent and a child. The block which has no parent is called the Genesis block of a particular chain. The “chaining process” entails the incorporation of the hash value of a parent block in the header of the child block. A block’s header contains all the metadata of the block. This linking of parent and child through a hashing process ensures

immutability of data of a child’s parent block and then all its ancestors up to the genesis block

Before explaining the components of a blockchain in more detail, we need to clarify the term “distributed ledger” and its connection, if any, to the concept of “distributed database”.

A ledger, primarily an accounting term, is a date-wise summary of all transactions of values, details of which are kept in a supporting book called “journals”. The word” ledger” was used in the blockchain context because its first use case was in the creation of a decentralized currency system. Since a ledger is also a record-keeping system, the term has persisted. But the question remains whether a ‘distributed ledger” is conceptually and practically equivalent to a “distributed database”. The answer is a big No.

Let us first demystify the term “distributed”. Oracle has defined a distributed database as “a set of databases stored on multiple computers that typically appears to applications as a single database. Consequently, an application can simultaneously access and modify the data in several databases in a network”.

Ozsu and valduriez have defined a distributed database and database management system as a “ Collection of multiple, logically interrelated databases distributed over a computer network. A distributed database management system (distributed DBMS) is then defined as the software system that permits the management of the distributed database and makes the distribution transparent to the users” (page 3). It is important to note that a distributed database system must also have an associated database management system to enable end users to access, query ,and generate user defined reports. Although a key-value database is also called a database, it provides limited support for data manipulation to discover patterns within the database and, therefore, the DBMS associated with it is very rudimentary.

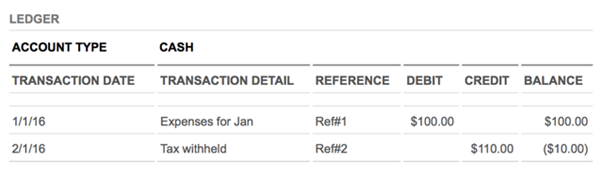

Let us now look into the ledger aspect of blockchain-based databases. What does a business ledger look like? IBM, while highlighting the deficiencies of current business ledgers, has given the following example.

IBM states that the current business ledgers are “inefficient, costly, and subject to misuse and tampering.” If this is the “reality”, then all the balance sheets and P&L accounts of IBM itself are faulty, and cannot be trusted by investing public as well as any tax authority”. Be that as it may, it is undoubtedly true that no enterprise will maintain its transactions only in a blockchain database although the immutability property of blockchain may have its own use.

For pedagogical purpose, let us consider the following example of an accounting database model

Obviously, a proper industry standard accounting information system (AIS) software will require a much more complex database. For our limited purpose, it suffices to note that a ledger book database cannot be a list of transactions only. A number of complex rules must be enforced on the database to create a proper double-entry accounting system. For example, a bank reconciliation process that matches a company’s bank statement with its cashbook balances is automated in many accounting information systems(AIS). The participants in this process must be authorized and cannot be anonymous validators. A blockchain-based database cannot be a solution for such essential requirements of an AIS, although underlying transactions can be stored in a private blockchain for future auditing requirements (see the article: Blockchain as the Database Engine in the Accounting System).

Let us consider the information management issues in regard to the Letter of Credit (LC), the most important banking document for facilitating international trade. In general, there are 5 five parties involved in an LC-based international payment settlement process. They are- importer, exporter, issuing bank, advising bank, and confirming bank. Today, banks use the SWIFT platform’s category 7 message type for sending and receiving messages between these parties. It is eminently possible to use a permissioned blockchain platform for sending and receiving LC-related messages. But it is impossible to use a public blockchain platform for this purpose. Furthermore, such a blockchain must rest at the top of a standard relational database to enable payment settlement and recording of underlying credit flow.

The moot point is that a blockchain-mediated database is extremely useful for record-keeping purposes and not for enabling contestable transactions involving values between a network of legally connected parties. For enforcement of any contract between two parties, the foremost requirement is the identification of the parties involved. It is immaterial whether the parties are connected in a network managed by a centralized authority or not. The anonymity of transacting parties should be considered the weakest part of a blockchain-based transaction system and not its strongest one. As we know a chain is as strong as its weakest part.

References:

References:

Musa Aujara Shamsuddeen (April 2019) ,Documentary Letter of Credit Discrepancy and Risk Management in the Nigerian: Crude Oil Export; Ph.D Thesis submitted to University of Central Lancashire

Özsu M. Tamer & Valduriez Patrick (2011) Principles of Distributed Database Systems; 3rd Edition 2011

Tan Boon Seng , Kin Yew Low (2019) Blockchain as the Database Engine in the Accounting System in Australian Accounting Review No. 89 Vol. 29 Issue 2

Distrust in fiat currency, controlled by a state, was one of the principal motivations in designing of the Bitcoin protocol. It was designed to be a decentralized system of creation of new money by a transparent computational algorithm. Any person participating in the currency’s ecosystem can run this algorithm on a computer and generate new money. It is supposed to be a currency created by the people for the people and therefore a currency of the people. It is a currency of future when true democracy will prevail. hereherehereherehere

But what is the reality? Who owns the bulk of these virtual currencies? To get an answer to this question, I looked into data about the distribution of these currencies amongst the participants in this technology game. The result of this exercise is truly revealing.

Data: We have collected data from the website https://bitinfocharts.com/top-100-richest-bitcoin-addresses.html which gives “Rich List” of some selected 9 currencies. We collected data as on 11th April, 2018. The market cap of these 9 currencies was 58.8 per cent of total market capitalization in terms of US dollar on that date. On the data date, the total market capitalization of virtual currencies (excluding tokens) was 261 billion US dollar. So one can say collected data is adequately representative of the virtual currency ecosystem. The website has grouped data by value of coins held against each address. An address having , say 0.001 bitcoin (BTC), would be grouped in the bucket “0 to 1 BTC” bucket. For some cryptocurrencies , the number of coins held in an address may be very large as their market value is much smaller as compared to that of Bitcoin. So the number of class intervals for coins held would be higher than a highly valued cryptocurrency like Bitcoin. To keep the results compact we have collapsed crypto wise class intervals into a common 3 classes. The following table gives a summary of distribution of value in US dollar and number of addresses across these class intervals.

Table 1: The distribution of addresses in terms of value of coin held and number of addresses for various class intervals of value of coins for each address.

Coin Name

Market Cap

$Billion

Share of each group of addresses below in total number of addresses

Share of each group of addresses in total market value of outstanding coin in USD

Average

Balance

(USD) per address

<=1 full Coin per address

1 -100 coins per address

More than 100 coin

less than or equal to1Coin

1-100 coins per address

> 100 coins

Bitcoin

130.3

4.06%

34.29%

61.7%

96.8%

3.1%

0.1%

5991

Bitoin cash

12.1

2.5%

27.6%

69.9%

97.1

2.8

0.1

737

Litecoin

6.8

0.4%

13.8%

96.7%

71.5%

27.1%

1.4%

2721

Dash

2.7

0.7%

9.4%

89.9%

82.0%

16.9%

1.2%

4094

Bitcoin Gold

0.8

2.9%

30.1%

67.0%

97.2%

2.7%

0.1%

38

Dodgecoin

0.4

0.0%

0.0%

100.0%

16.5%

42.2%

41.3%

183

ReddCoin

0.1

0.0%

0.0%

100.0%

14.8%

18.9%

66.3%

1317

Verticoin

0.1

0.0%

3.3%

96.7%

38.1%

47.1%

14.8%

715

Peercoin

0.0

0.0%

1.3%

98.7%

56.4%

32.0%

11.6%

934

It is obvious from the above table that only few addresses, each having more than 100 coins per address account for the bulk of total market capitalization of each currency. Bitcoin which the highest market capitalization of all circulating coins is also concentrated in a small number of addresses. The table 2 below clearly indicates how a few big market players have completely taken over each currency market.

The US tax authorities as well as Commodity Future Trading Commission have designated as “commodity” and not currency. From that perspective, this commodity market is highly monopolistic and susceptible to market manipulation by few large traders. It is high time that anti-trust authorities in the developed economies wake up to this reality and take appropriate actions in the interest of average participant in these markets.

Table 2: The number of addresses and value held by top bracket by number of coins held per address

Coin Name

Number of addresses in the highest bracket

Market value of coins held by addresses in the top bracket (million USD)

Share of these addresses in outstanding market value of the respective Coin

Key words: Central Bank Digital Currency, public key-private key cryptography, Digital currency wallet, Corruption,

Introduction: No currency has ever been used in the human history which did not have the stamp of an authority. Bitcoin is a medium of payment but it is not money for the same reason. Nonetheless, the technology underlying Bitcoin is a significant one with great potential. A central bank, issuer of paper currency, can use some selected components of Bitcoin technology to replace paper currency with virtual currency, retaining all the important features of paper currency. The most important of them is that a central bank note is a freely negotiable bearer bond and a legal tender in the hand of its holder. It does not require any third party verification. Counterfeiting a central bank note is not impossible but difficult and costly. The central bank neither authenticates any transaction made with that particular note nor does it keep any record of that transaction. The note remains as a liability on the book of the central bank till it comes back to it, either for reissue or its destruction. The physical nature of the note ensures that no double spending is possible with the same note by its current holder. In case of digital cash, the main issue that a central bank has to resolve is the issue of double spending without depending on third party verification of the same. What follows hereunder is an outline of a system that any central bank can implement to issue its own currency retaining most, if not all, of the desired properties of a paper currency.

I am presenting below a system based on digital currency on a mobile phone. There is no compelling reason to believe that the same system cannot be implemented on a specially designed smart card with embedded chip. The system outlined below is described within the currency management framework of the Reserve bank of India (RBI). With little tweaking the same can be customized by any central bank.

RBI Currency Management Framework:

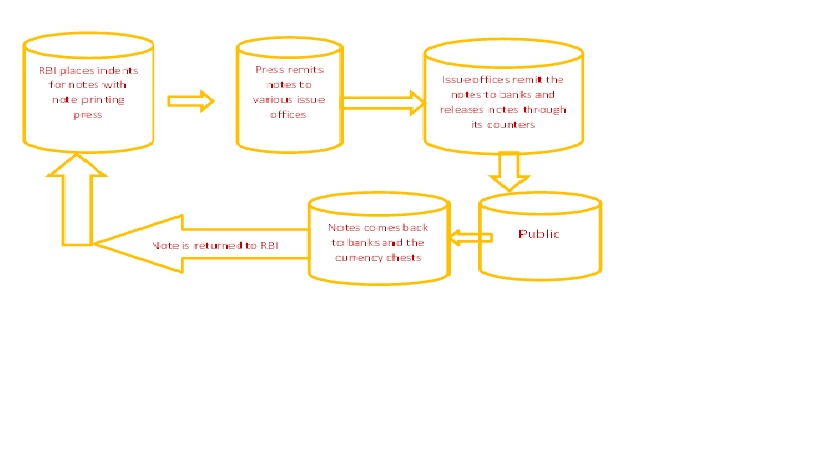

RBI carries out its currency management function through its 19 Issue Offices located across the country. There is a network of 4281 currency chests and 4044 small coin depots in selected commercial bank branches. These chests store currency notes and rupee coins on behalf of RBI. The note distribution mechanism is summarized in the following diagram.

For issuance of digital currency, each currency chest would function as a data center for hosting the ledger book of notes issued from it. Similarly each issue office of RBI would have a copy of the entire ledger book of notes. A folio would be opened in the note ledger book when the first time a specific note is issued. Each data center will have complete inventory of wallets issued by RBI.

Every bank branch would have a digital cash dispenser. Any wallet holder would be able to replenish her wallet with digital currency by pairing it with the dispenser via Bluetooth or NFC communication channel. Similarly every ATM would have similar facility. At the time of cash dispensation from bank branch or ATM would require Aadhaar based biometric verification of wallet. For cash transfer between wallets of two individuals this verification is not a necessary requirement.

The protocol for issue of eRupiah

RBI would maintain ledgers of each currency note in a distributed database.

Currently RBI issues notes through its Issue offices. The distributed database will be created according to issue departments of RBI. Each Issue office of RBI will be able to issue new digital currency and destroy old digital currency. Destruction of old digital currency would help RBI to keep the number of entries in the ledger folio of a particular note within a limit. Every Issue offices would maintain record of all notes issued by it as well as copies of corresponding records of 3 neighboring Issue offices.

Each currency chest will have a database of notes received by it from RBI’s Issue department.

Each currency chest will also have replicated database of its three nearest neighbor

The system will issue new digital currency when an account holder wants to withdraw cash from its account with RBI.

The account holder would specify how much of its cash withdrawal would be in digital form. This facility would be provided for an interim period when both forms of currency would be in circulation.

To incentivize issue of digital cash, RBI may reward with a fixed amount that could be related to the cost of producing physical cash.

RBI is banker to the Central and State Governments. It also functions as banker to the banks and thus enables settling of inter-bank obligations. These account holders of RBI would get digital cash in their Jumbo Wallet which would be a server in the account holder’s custody. It would be like a till holding cash. An authorized person can withdraw e-Rupiah from the till as and when required.

The RBI’s Note ledger would comprise ledger folios of each currency notes issued.

Each record in the Note ledger would comprise the following attributes: (1) a sequential no, (2) unique identity / sr no of a note, (3) hashed value of the note serial no, (4) identity of the issue department, (5) denomination, , (6) time stamp of transaction, (7) hashed value of identity of paying wallet (first time payer would be RBI), (8) hashed value of identity of receiver wallet, (9) active flag, (10) hashed value of first 9 attributes , (11) hash value of the first 9 attributes of earlier transaction record of the same note. The identity of a wallet is described below.

RBI will also maintain database of each wallet downloaded from its website.

The wallet database will have a header record with the following attributes (1) IMEI no of each phone, (2) Aadhaar No of the phone owner, (3) timestamp of successful downloading of the wallet, (4) the GPS location of the phone at the time of downloading of the wallet, (5) a unique private key generated for each wallet and (6) the corresponding unique public key generated for each wallet. This data would also be hashed and encrypted with RBI’s private key and will be part of the header record. RBI’s public key would also form a part of the header record. The private and public key of each wallet would be generated by RBI at the runtime. The hashed value of attributes 1 to 6 would be the identity of each wallet.

Each wallet will have its own database of transactions. Each record in the transaction database will represent a note that has been loaded into the wallet. Each record will have the following attributes: (1) unique identity of the note, (2) note denomination, (3) digitally signed (with the private key of the paying wallet) hashed value of the concatenated string of serial no and denomination, (4) digitally signed ( with the private key of the paying wallet) hash value of concatenated string of attributes 1 and 2 of the header record with private key of payer wallet, (7) public key of the paying wallet, (8) timestamp of last transaction( i.e. timestamp of receipt of the note , (9) timestamp of the payment transaction, (10) payment status (paid or unpaid), (10) hashed value of the earlier transaction of the note(attributes 1,2,3,4,5).

A transaction between two wallets would involve “note data” transfer from the paying wallet to receiving wallet. Every note that gets transferred from the payer’s wallet to the recipient’s wallet would essentially mean transfer of the entire record from the former to the latter. In the process of data transfer two insert / update activities take place in the receiver’s and payer’s wallet respectively. The receiver’s wallet inserts a new note record while the payer’s wallet updates the concerned note’s existing record.

Once the receiving wallet gets a new e_Rupiah note, it checks the authenticity of the note by calculating hash value of the concatenated string of attribute 1 and 2 of step at 13. In the payer’s wallet the status flag would get changed to “paid” while in the receiver’s wallet it would continue to have the status flag as “unpaid”.

Any wallet would have a limit in terms of number of records / notes. When the database has reached its limit then the wallet would have to be uploaded to RBI and a new wallet has to be downloaded.

At any point of time a single wallet would be subject to 2 limits- holding limit of no of transactional records and total value of a single transaction. For a high value transaction two factor authentications would be required. (say above one lac). Both paying wallet as well as receiving wallet has to simultaneously establish connection with RBI and get their credential verified.

As and when no of records in a wallet’s transactional database reaches its limit, the database has to be downloaded in an ATM or at a bank branch. The wallet would be purged of the all transaction records with status as “paid”. The wallet holder then can download more E_Rupiah from an ATM or from a bank brunch. RBI will update its ledger book of individual notes thus uploaded from each wallet.

Any fraudulent transactions identified in the process of uploading would get notified and thorough automated forensic audit perpetrator of fraud would get identified.

One of the fundamental lessons of all financial scams is that there always exists enough number of gullible people to be conned by merchants of dream. For example, the people of 17th century Amsterdam started believing that prices of a bunch of tulip bulbs could rise to a level higher than the value of a furnished luxury house. It also happened during the dotcom bubble of late 1990s. Presently such a bubble is unfolding before our own eyes and the sad part of it is that some financial sector regulators are actively encouraging formation of this bubble in the name of financial innovation. It would be apposite here to recall the scathing criticism that the Financial Crisis Inquiry Commission of US Congress made of the regulatory failure leading to the sub-prime financial crisis: We conclude widespread failures in financial regulation and supervision proved devastating to the stability of the nation’s financial markets.

U.S. financial firms CME Group and CBOE are going to launch Bitcoin futures on December 18, followed by launch of binary options on Bitcoin by Cantor Fitzgerald. The US regulator for futures market, Commodity Futures Trading Commission (CFTC), has allowed introduction of these new products by these exchange platforms on the basis of self-certification submitted by them. The Commodity Exchange Act of USA allows such exchanges called Designated Contract Markets (DCM) to introduce new contracts by submitting a written self-certification to the CFTC that the contract complies with the Commodity Exchange Act (CEA) and CFTC regulations. It is the responsibility of DCMs to determine that the offering complies with the CEA and Commission regulations.

The CFTC in its press release of 1st December has referred to the IRS characterization of Bitcoin as a virtual “currency”. More than that, IRS has referred it as “convertible virtual currency”. I have already explained in my earlier blog why Bitcoin cannot be called a currency. In 2015, CFTC declared Bitcoin as a “commodity” by referring to the CEA act that includes “all services, rights, and interests in which contracts for future delivery are presently or in the future dealt in.” in the definitional boundary of commodity. The press release clarifies that “Bitcoin and other virtual currencies are encompassed in the definition and properly defined as commodities”. Under CEA commodities are classified into three categories-

(1) Agricultural commodities

(2) Excluded commodities which include, inter alia, an interest rate, exchange rate, currency, security, security index, credit risk or measure, debt or equity instrument, index or measure of inflation, or other macroeconomic index or measures

(3) Exempt Commodity which means a commodity that is not an excluded commodity or an agricultural commodity.

Prof. Shadab of New York Law School has argued in his written statement submitted to the CFTC that Bitcoin should be classified as “exempt commodities and not as excluded (currency) commodities “.

Each Bitcoin future contract on CME would be composed of 5 Bitcoins. The tick size (the minimum fluctuation) has been fixed at $5 per bitcoin, amounting to $25 per contract. Per person open position limit has been set at 1000 contracts. The daily price fluctuation of a Bitcoin future is limited to a 20% band above or below the prior settlement price. The settlement price will be Bitcoin Reference Rate (BRR). BRR is calculated by UK based crypto currency trading platform -Crypto Facilities Ltd, in partnership with CME. BRR is calculated by taking traded price and volume data from a few selected exchanges involved in spot Bitcoin trading. Price and volume data are obtained for 12 periods of 5 minutes each in the last hour of trading. For each time interval, a volume weighted median price is calculated. The overall price is average of these 12 prices.

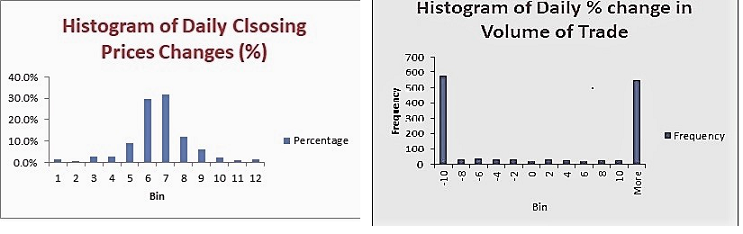

So, purely from methodological perspective, construction of reference price cannot be faulted. Since BRR is based on observed prices of Bitcoins traded on mostly unregulated exchanges, these prices are always subject to manipulation. The extent of volatility that can happen on these exchanges can be understood from the movement of bitcoin price on December 7. On this day, the price of 1 Bitcoin fluctuated from a high of USD 19,000 to a low of USD 4,000. If the price volatility is considered in conjunction with volume volatility (see the graphs below), Bitcoin may turn out to be Twenty First century’s first virtual Tulip.

Given this “insane volatility” ( as described by the chairman of BBCBS committee) of spot prices of a traded asset, the CFTC’s move in allowing derivative products on such an asset can be highly counterproductive. Apparently the CFTC believes that by bringing Bitcoin on a regulated platform it would be able to contain the speculative excess. The high margin requirement is expected to dissuade small investors to take positions in the Futures market, leaving the field open for play by institutional investors. More than 100 hedge funds have been created in the last one year to trade in digital currency only. It is reported that there is $10B of institutional money waiting on the sidelines to invest in digital currency today. To meet the requirements of these institutional investors, Coinbase, the US based Bitcoin exchange, has launched a new company to store securely their digital assets (see here). The company has claimed that it is already holding $9 billion of digital currency on behalf of its customers.

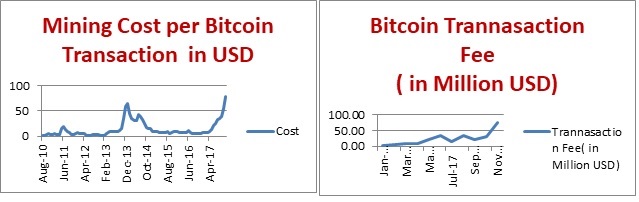

It should be a matter of regulatory concern about the source of Bitcoin’s price volatility. Apart from alleged price manipulation the most plausible explanation would be the intrinsic unbridgeable gap between demand and supply of Bitcoin. New supply of Bitcoin is largely a result of mining activities and the maximum supply of Bitcoin is a known figure. Against the back drop of a largely inelastic supply curve, the demand curve is driven by enthusiasts of cryptocurrency- a fast growing tribe. The fundamental inelasticity of the supply curve is getting reflected in higher and higher cost of Bitcoin based transactions. The following two graphs show how running Bitcoin network becoming costlier and costlier.

Given its inherent supply constraint, there is no possibility of Bitcoin becoming a global currency in its current form. Since Bitcoin is a highly sophisticated technological product, it attraction to young people is immense, like marijuana once was. But it should be the job of central banks to proclaim from the rooftop with as much force as it can command that: Trading and or Investing in Bitcoin is injurious to your financial health.

Digital currency is currently in news. Russia and China is reported to be on the verge of issuing official cryptocurrency. CME, the world’s largest exchange, is planning to introduce future on Bitcoin by the end of this year.HereHere In my last post I have explained why Bitcoin can be considered at best a currency of a community- a virtual country, so to say- of Bitcoin users. So a future on a foreign exchange of an unknown country without any verifiable foreign trade activities is definitely problematic. Be that as it may; the possibility of introducing digital currency by central banks is now a hot topic. The head of the Secretariat of the Committee on Payments and Market Infrastructure of BIS along with a colleague has recently published a paper on the Central Bank Cryptocurrencies. In this paper the authors have identified four key properties of Money- issuer (central bank or other); form (electronic or physical); accessibility (universal or limited); and transfer mechanism (centralised or decentralised). It is interesting to see that the authors have failed to identify the most important property of money- unit of account. A medium of payment is not a currency unless it is also a unit of account. That is why a credit card, a bank debit card or a prepaid cash card is not money, despite each being a digital medium of payment. In fact, in terms of volumes as well values, the medium of payments even in a developing country like India is largely electronic. The following table shows that money in India exists mostly in the digital form, as most of the bank money is. Even after exclusion of time deposit from the ambit of payment system, the digital money ( bank money) dominates the physical money or cash.

Composition of Broad Money (M3) in India

Currency with the Public

Deposit money of the public

Time Deposits with banks

9.84%

11.15%

79.01%

So issuance of central bank currency would only digitalize the cash component of money as other medium of payments are already in digital form. So CBCC should be considered only as a replacement of physical cash issued by a central bank. The champions of cryptocurrency, however, would like it to be the sole medium of payments, at least of the online variant. It is difficult to understand why anybody would like to replace a part of the system that is working fine with another only because of its compatibility with a particular ideology about issuance of money. In fact, instead of reducing the cost, a decentralized transfer mechanism like bitcoin would increase the social cost of running a payment system. Leaving aside these ideological issues about money for now, let us consider the possibilities of issuing cryptocurrency by a central bank. I intend to outline a protocol that can be adopted in the specific case of India. In this post I enumerate the essential features that a Central Bank Cryptocurrency Currency(CBCC) should possess with specific reference to India.

The Reserve Bank of India (RBI) spent on average 35 billion of rupees in printing notes in last 3 years, ignoring the spike of 2016-17 due to demonetization. This amounts to more than 500 million dollars- not a small sum. The commercial banks also have to incur huge cost over and above the printing cost incurred by RBI to manage the last mile of the currency supply chain. If we can replace printing of notes by creating digital strings of binary numbers in computers, the total cost could be easily reduced significantly. It is not necessary to eliminate physical cash completely. Digital and physical cash could coexist for a long time to come. When every citizen is connected to the digital space we can think of complete elimination of physical form of cash.

Let us first understand how the paper currency system works in India. Before that, we need to consider the enormity of logistics involved in cash management system in a country like India. As on end March 2016, 90 billion pieces of notes and 89 billion pieces of coins were in circulation in India. The number of currency chests and coin depot/sub-depot were 4211 and 4008 respectively at the end of 2012. There were around 222 thousand ATMs in India. The details of the currency supply chain is given below.

Note printing presses print notes as per indents placed by Currency Management department of RBI.One characteristic of the paper note is worth noting here; every note has a distinct identity.

RBI receives the currencies in their vaults

RBI remits the currencies so received to various currency chests maintained at bank branches.

The commercial banks run the currency chests as an agent of RBI, while the treasure in it is the property of RBI. Any withdrawal or deposit into the currency chest is recorded as debit or credit respectively in the bank’s account maintained with RBI.

Transport of currencies from currency chests to other bank branches is the responsibility of banks.

General public can obtain cash from banks either over the counter of bank branches or from ATMs. Government departments having accounts with RBI withdraw cash from RBI counters to meet their cash needs, and thereby inject cash into the economy.

When general public or government departments deposit cash into their bank accounts, the banks or RBI examine the circulation worthiness of deposited notes. The soiled notes are then withdrawn from circulation and briquetted by RBI.

We are interested in designing a supply chain that delivers digital currency to general public, maintaining the basic functionality and integrity of the existing supply chain. We need not differentiate between notes and coins in the digital environment. .

The main characteristics of the proposed CBCC would be as follows:

Each note would have specific denomination- large denomination of 5000 and 10000 can also be introduced.

If Alice wants to pay 102 rupees to Bob and Alice has only one 100 rupees and one ten rupees in her wallet, the system would function exactly the way cash based transaction would function. Alice would pay one 100 and one ten rupees to bob. Bob would immediately pay back to eight rupees to Alice in denominations available to Bob.

Like Bitcoin there would be wallets as app in mobile or users can use hardware based wallet also. There is no question of having any exchange as custodian of wallet in dematerialized form.

A person without a bank account can download a wallet and can receive digital currency in this wallet.

There would be no connection with a wallet with wallet holder’s bank account. However, a wallet holder would be able to download cash from her bank account as currently she withdraws cash from her bank account. The only difference would be that the bank / ATM would give her digital cash and not physical cash

There would be no special KYC verification for downloading digital wallet apart from providing a unique identification number.

In case of loss of a wallet, the process would be the same as it happens if one losses one’s physical wallet containing physical cash. A First Information Report (FIR) has to be registered with a police station and the system would ensure that missing digital notes are blocked to the extent the digital money in the lost wallet has not been spent till that time. After completion of investigation the cash can be restored to the original owner.

The central bank may prescribe a limit to the value of digital currency a wallet can hold. For example, it may be stipulated that the wallet is designed to hold a maximum amount of 100 K rupees. A wallet holder would not be able to load cash to her wallet from a bank or from another payer more than amount.

It may be possible to take insurance for loss of a wallet with a sum insured to the extent of a pre-determined fraction of the amount lost. The wallet holder has to pay the insurance premium.

It would be issued by the central bank as it is done today.

It would retain the anonymity of cash to a large extent- but theoretically for a given transaction payer and recipient’s identity can be found out.

There would be almost instant authentication of any transaction without any third party verification. The central bank would take the responsibility of authentication without any manual intervention. The process would be almost instantaneous as it happened in the use of debit card today.

It would run parallel to paper currency till such time the share of paper currency becomes negligible

It would be a legal tender with the rider that if the recipient of a transaction is not ready to accept digital currency, the payer has to pay the former with paper currency.

All government agencies would have the infrastructure to receive digital currency. No government agency or a public utility would not be able to deny any digital currency transaction if the counterparty insists on that form of transaction. Thus a citizen would be able to buy a bus or metro ticket with digital currency. Taxes also can be paid by digital currency.

A bank account holder can go to a bank branch or an ATM and would be able to load digital currency in her wallet as if physical cash is being dispensed as it happens today.

With the consent of its employees, an employer can pay wages or salaries in the form of digital currencies. Government would prefer to give subsidies through digital currencies.

Digital currencies would not work outside the jurisdiction of the issuing central bank. Thus it is a legal tender within the country of issuing central bank.

A foreign citizen can exchange foreign currency with digital currency as long as he or she gets the wallet downloaded from the issuing central bank’s portal. The only restriction is that if the wallet is used for transaction outside the issuing central bank’s jurisdiction, it would not be authenticated. A money changer can exchange foreign currency (paper form) with domestic digital currency.

No transaction fee is to be paid for using digital currency

The central bank would be free to issue digital currency of any amount as it happens today.

Is it possible to have CBCC with all the above features? Surely it is possible using the same technology that Bitcoin uses, with some tweaking. In my next post I will outline a high level design of such a system. I am confident that it should be possible to develop such a system which would not allow double spending and provide a very high level of anonymity to transactors and their transactions.